India Diagnostic Market Overview

India's diagnostic sector is at an inflection point. The convergence of a rising disease burden, a healthcare system actively scaling its infrastructure, and a technology wave transforming how tests are ordered, processed, and reported is creating one of the most compelling growth stories in Asia's healthcare economy. What was once a fragmented, largely unorganized market is rapidly consolidating into a sophisticated, data-driven ecosystem serving hundreds of millions of patients across urban centres and emerging tier-2 and tier-3 cities alike.

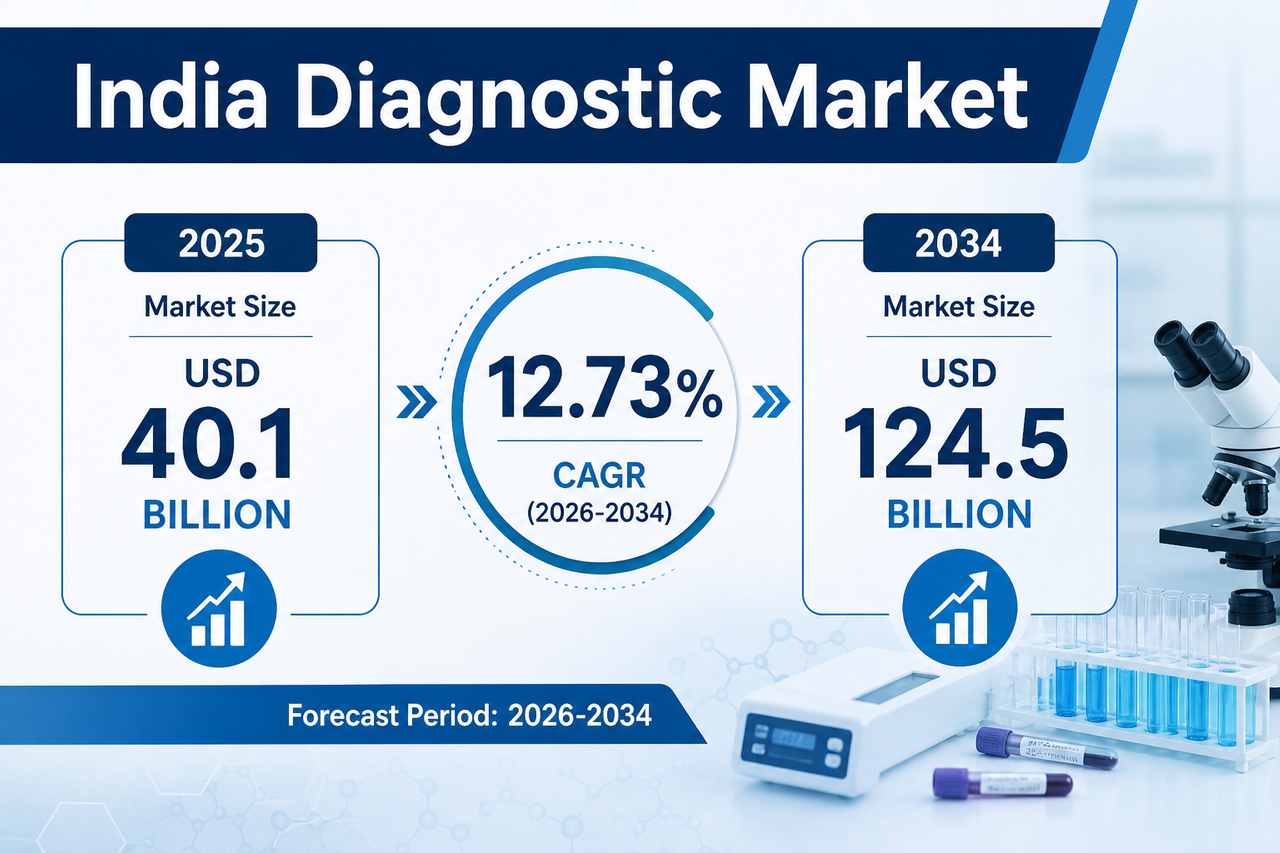

The diagnostic market size in India was valued at USD 40.1 Billion in 2025 and is projected to reach USD 124.5 Billion by 2034, with a compound annual growth rate (CAGR) of 12.73% during the forecast period 2026-2034. This growth is driven by increasing chronic and infectious diseases, rising healthcare awareness, expanding infrastructure, and advanced diagnostic technology adoption. The market includes hospitals, laboratories, and imaging centers, with government initiatives boosting detection and patient outcomes.

Market Statistics-At-A Glance

- Current Market Size (2025): USD 40.1 Billion

- Projected Market Size (2034): USD 124.5 Billion

- CAGR: 12.73%

- Clinical chemistry dominates the market with a 32.8% share in 2025.

- Reagents and kits lead the product type segment with a 67.4% market share.

- Infectious disease application holds the largest share at 29.6%.

- Diagnostic chains represent the largest end-user segment with 38.9% share.

- West India region leads with 31.2% share, supported by strong healthcare infrastructure.

Key Drivers Behind India Diagnostic Market Growth

- Proliferation of Point-of-Care Testing: A significant growth driver is the rapid adoption of point-of-care testing (POCT) solutions that deliver quick results outside traditional laboratory settings. In September 2025, Bartronics India planned to invest up to INR 50 Crore to acquire an initial 15% stake in Huwel Life Sciences — strengthening point-of-care testing, ICMR-approved molecular diagnostics, and the global deployment of rapid infectious disease solutions. POCT devices for glucose, cardiac markers, infectious diseases, and pregnancy testing are increasingly deployed in clinics, community health centers, and mobile health units, making decentralized diagnostics a key driver of improved care accessibility across urban and rural regions.

- Digital Transformation and Laboratory Automation: Digital transformation is reshaping India's diagnostics landscape through extensive laboratory automation, including sample tracking systems, auto-analyzers, and integrated laboratory information systems. These technologies improve operational efficiency, reduce turnaround times, and minimize human error — enabling higher test volumes with consistent quality. Diagnostic centers are investing in sophisticated IT infrastructure to unify workflows, support real-time reporting, and enhance interoperability with hospital systems across multi-site networks.

- Rising Demand for Preventive Health Screening: The growing emphasis on preventive health screening driven by both public and private initiatives, promotes early detection of chronic conditions including diabetes, hypertension, and cancer. Affordable screening packages offered by diagnostic chains and hospitals encourage routine check-ups among working populations. Employers, insurers, and wellness programs increasingly support comprehensive health screening, enhancing market penetration and fostering a proactive approach to long-term disease management.

- Rising Chronic and Infectious Disease Burden: Non-communicable diseases contribute to 53% of all deaths in India and account for 44% of disability-adjusted life years, according to the Department of Biotechnology. Cardiovascular diseases alone account for approximately 31% of all fatalities. India's tuberculosis incidence stood at 187 cases per lakh population in 2024. This dual burden of chronic and infectious disease is creating sustained, high-volume demand for diagnostic testing across hospitals, laboratories, and diagnostic chains nationwide.

Evaluate Market Opportunity Before Investing - Request for a Sample Report

India Diagnostic Market Outlook (2026–2034)

The India diagnostic market is poised for sustained and accelerating growth over the forecast period. Expansion of organized diagnostic chains into tier-2 and tier-3 cities, rising demand for personalized medicine, and the scaling of point-of-care and home diagnostics are expected to create significant new revenue streams. Continued government support through preventive healthcare initiatives, public-private partnerships, and regulatory modernization will enhance accessibility and affordability. Ongoing innovation in digital reporting, laboratory automation, and AI integration is projected to streamline diagnostic services at scale propelling the market from USD 40.1 Billion in 2025 to USD 124.5 Billion by 2034, at a CAGR of 12.73%.

Segmentation-Wise Market Breakdown

➤ Clinical Chemistry dominates by type at 32.8%, owing to its widespread application in measuring metabolites, enzymes, and electrolytes for preventive, diagnostic, and therapeutic purposes. Hospitals and diagnostic centers favor clinical chemistry analyzers for high-throughput testing, automation capabilities, and standardized workflows. The increasing prevalence of diabetes, cardiovascular disorders, and liver dysfunction further drives sustained demand for clinical chemistry testing.

➤ Reagents and Kits lead by product type at 67.4%, supported by wide application across clinical chemistry, hematology, immunology, and molecular diagnostics. Standardized reagent kits ensure accuracy, reproducibility, and efficient workflow integration — making them indispensable for hospitals, laboratories, and diagnostic chains. Manufacturers are enhancing reagent stability and providing multi-purpose kits compatible with various analyzers to sustain dominance.

➤ Infectious Disease leads by application at 29.6%, driven by the high prevalence of tuberculosis, hepatitis, and vector-borne infections. Government screening programs, rapid diagnostic initiatives, and the adoption of molecular assays and immunoassays have significantly increased testing demand, while urbanization and seasonal outbreaks sustain market demand throughout the year.

➤ Diagnostic Chains account for the highest end-user share at 38.9%, leveraging extensive networks, operational efficiency, and investment in automated testing infrastructure to handle large patient volumes with consistent diagnostic accuracy. Integration of advanced laboratory management systems, tele-diagnostics, and home sample collection services continues to expand their market presence.

➤ West India leads by region at 31.2%, with Maharashtra and Gujarat hosting large hospitals, reference laboratories, and diagnostic chains that drive high testing volumes. In November 2025, MedGenome acquired a majority stake in Gujarat-based Green Cross Genetics Lab, combining genomics-led precision testing with an integrated network of 17 labs, 35 collection centres, and 800+ diagnostics nationwide.

Key Market Challenges

- Inconsistent Quality Standards Across Facilities: A significant challenge is the lack of uniform quality standards across laboratories and diagnostic centers. Variability in testing protocols, equipment calibration, and quality control practices leads to inconsistent results, undermining clinical confidence. Smaller and independent labs often lack accreditation due to the costs and complexity of compliance hampering nationwide standardization and increasing the need for stronger regulatory oversight.

- Infrastructure Gaps in Rural and Semi-Urban Regions: Infrastructure limitations in rural and semi-urban areas remain a key restraint on market growth. Many regions lack fully equipped laboratories, trained technicians, and reliable connectivity required for modern diagnostics. Patients often travel long distances for basic tests, delaying care and increasing out-of-pocket expenses. Targeted investment in mobile diagnostic units and scalable solutions is critical to improving healthcare equity nationwide.

- High Cost of Advanced Diagnostic Technologies: The high cost of acquiring and maintaining advanced technologies including next-generation sequencing, automated analyzers, and high-resolution imaging systems presents a major barrier for smaller healthcare providers. Expensive consumables and service contracts increase ongoing operational costs, constraining widespread adoption of cutting-edge diagnostics and reinforcing reliance on conventional testing modalities across cost-sensitive segments.

Competitive Lanscape - By IMARC GROUP

Gain comprehensive access to an in-depth analysis of the competitive landscape, including market structure, key player positioning, competitive dashboards, winning strategies, and detailed profiles of all major industry participants within the full research report.

Top Players in India Diagnostic Market:

- MedGenome

- Mahajan Imaging

- Bartronics India

- Huwel Life Sciences

- Fujifilm India

- Cipla

- Amazon India (in diagnostics service context)

India Diagnostic Market - Recent News

- In January 2026, Fujifilm India introduced advanced medical imaging and healthcare IT solutions including the AI-powered FCT iStream CT scanner, digital mammography, X-ray equipment, and HCIT Fenix system enhancing diagnostic accuracy and operational productivity.

- In November 2025, Cipla launched India’s first integrated Breathefree Lung Wellness Center in Delhi offering over 60 advanced lung diagnostic tests aimed at improving respiratory health through early diagnosis, rehabilitation, and research.

Discuss Your Requirements With an Analyst and Get Your Customized Market Report

Note: If you require any specific information not covered within this report’s scope, we will provide it as part of the customization.

Conclusion:

A comprehensive analysis of the India diagnostic market highlights a clear shift toward a more technology-driven, accessible, and patient-centric healthcare ecosystem. Rising disease burden, increasing health awareness, and expanding medical infrastructure are accelerating demand for accurate and timely diagnostics. At the same time, advancements in molecular testing, automation, and AI-enabled solutions are enhancing efficiency and clinical outcomes.

IMARC Group’s insights indicate that organizations investing in advanced technologies, nationwide network expansion, and digital integration are likely to strengthen their competitive positioning. This evolution reflects more than strong market growth it signals a structural transformation toward a scalable, innovation-led, and prevention-focused diagnostic ecosystem across India.

Verified Source: IMARC Group

Contact Us

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel: (D) +91 120 433 0800

United States: +1-201971-6302